How Supabase Built a $2 Billion Firebase Alternative - With a Small Team and an Open-Source Bet

I spent two days digging through investor memos, founder interviews, Craft Ventures' inside account, and every public data point I could find on Supabase's growth. After reading 50+ threads, three long-form strategy pieces, and tracing the product's revenue curve from $1M to $16M in four years, one thing became impossible to miss: this is not a typical VC-backed scaling story. It's a slow-compound product-and-community machine that eventually went vertical when AI vibe coding created a new category of backend demand overnight.

Here's what actually happened, and what you can take from it.

The Setup: Firebase Had a Problem It Couldn't Fix

Google's Firebase was the go-to backend for mobile and web developers for years. Real-time database, auth, storage, hosting - all in one platform. It worked. Millions of developers loved it.

But it had two structural weaknesses that Google couldn't fix without breaking what made it popular.

First: vendor lock-in. Firebase uses a proprietary NoSQL document model. Once you build on it, migrating is painful. Developers hate being trapped.

Second: no relational database. Firebase's Firestore is flexible but can't do real relational queries. As products grew and data models got complex, founders kept hitting walls Firebase wasn't designed to solve.

Paul Copplestone saw both of these problems clearly. He was a developer himself - not a startup guy who spotted an opportunity. He was someone who wanted Postgres and kept wishing Firebase existed for it. So he built what he wanted.

That authentic founder-user alignment isn't a marketing strategy. It becomes one.

How It Started: Y Combinator, 2020

Paul Copplestone and Anthony Wilson founded Supabase in 2020 and immediately went through Y Combinator. The pitch was simple: open-source Firebase alternative, built on PostgreSQL.

PostgreSQL - or Postgres - is the world's most popular open-source relational database. It has a massive existing developer community, decades of documentation, and native SQL support. Building Firebase's ergonomics on top of Postgres wasn't a technical moonshot. It was a genuinely useful wrapper that saved developers weeks of setup time.

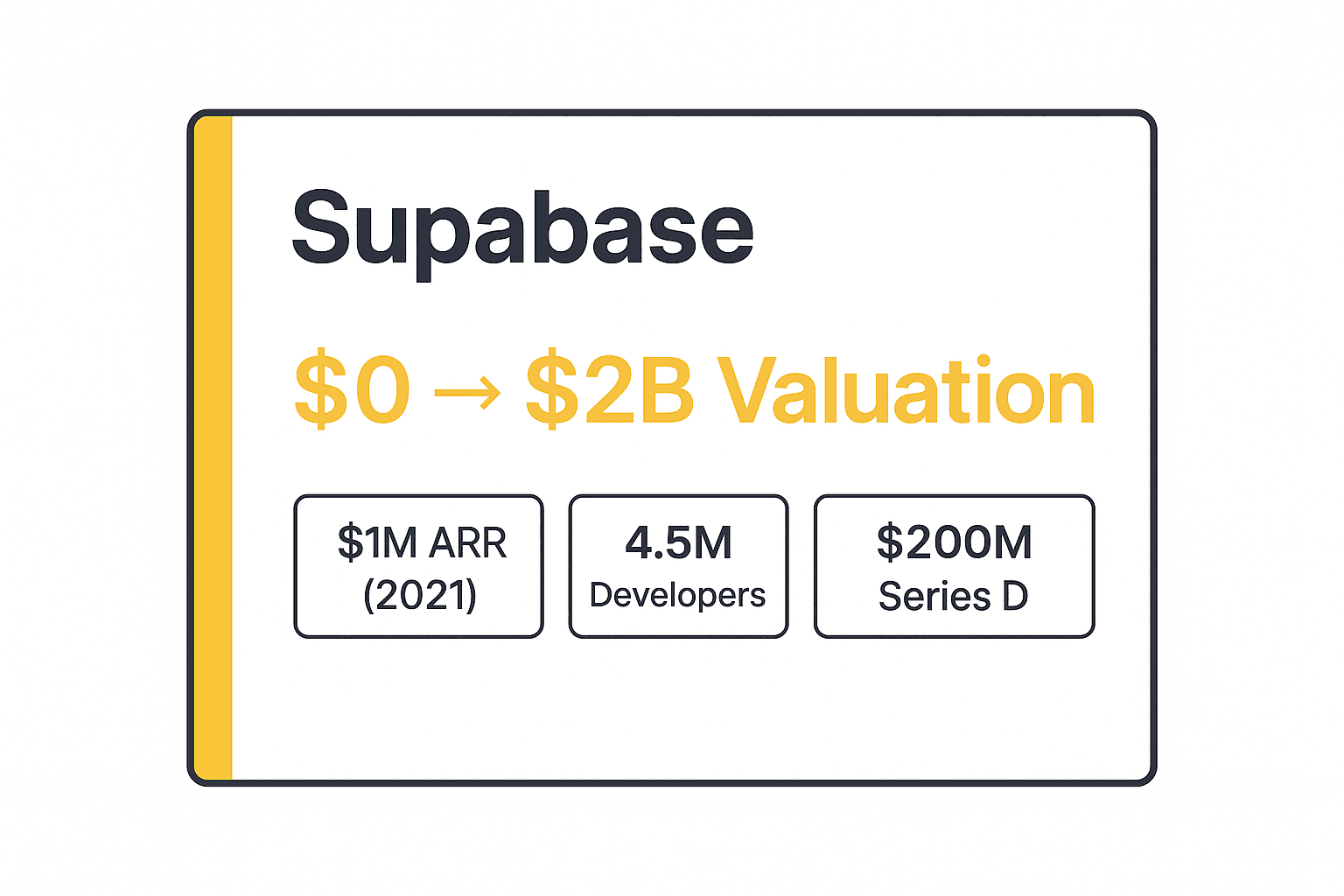

In August 2020, they raised a $125K pre-seed from Y Combinator. By December, Coatue led a $6M seed round.

The early product was minimal but compelling: a Postgres database with a real-time API layer, auto-generated REST and GraphQL APIs, auth built in, and file storage. Everything Firebase provided, but on open source infrastructure you could self-host if you wanted, or run on Supabase's managed cloud.

Open source was the product-market fit signal. Not just for flexibility - for trust. Developers could read the code, audit the security, deploy it themselves. That transparency became the moat.

Revenue Growth: $1M to $16M in Four Years

Here's the arc:

| Year | Revenue |

|---|---|

| 2021 | $1M |

| 2022 | $6M |

| 2023 | $11M |

| 2024 | $16M |

| 2025 | $27M (projected) |

The funding story matches the revenue:

- October 2021: $30M Series A (Coatue)

- May 2022: $80M Series B (Felicis)

- September 2024: $80M Series C at $0.9B valuation (Peak XV + Craft Ventures)

- April 2025: $200M Series D at $2B valuation (Accel)

The Series D came with an unexpected validator: James Tamplin, the co-founder of Firebase itself, was an early angel investor in Supabase. When the person who built the thing you're replacing bets on you, that's a meaningful signal.

The Product-Led Growth Engine

One of the most important moments in Supabase's growth story came when Craft Ventures embedded their Operator-in-Residence full-time at the company. The task: codify what was already working into a repeatable system.

What they found: Supabase had a clear activation event. Everything before it was noise. Everything after it compounded.

The activation event: getting a database created.

Not signing up. Not exploring the dashboard. Not reading docs. The moment a developer created their first Postgres database on Supabase, something changed. Their likelihood of converting to paid, returning the next week, and eventually becoming a power user jumped dramatically.

That single insight drove the entire lifecycle design: get new signups to database creation as fast as possible. Reduce every click, every friction point, every moment of confusion that stood between "I just signed up" and "I have a running Postgres database."

This is a masterclass in growth clarity. Most founders optimize for sign-up volume. Supabase optimized for the specific moment that actually mattered.

The Two ICPs That Required Different Journeys

Craft's embed also uncovered a segmentation problem that was quietly causing friction.

Supabase had two distinct user groups entering the product:

Postgres-familiar developers - engineers who'd used relational databases before and instantly understood what they were getting.

Developers new to databases - especially frontend and mobile developers who'd been using Firebase and were comfortable with document models but had never written a SQL query.

These groups needed completely different onboarding journeys. The Postgres-familiar developer didn't need a tutorial on relational thinking. They needed speed-to-running-database. The Firebase convert needed a mental model shift first.

Treating them identically - which is what most products do with a single onboarding flow - meant either going too fast for beginners or going too slow for experts. Bifurcating the lifecycle to serve them separately was one of the unlocks that drove the 1M-to-4.5M developer jump.

Most founders have 2-3 distinct ICP types and one shared onboarding. That mismatch is usually invisible until someone looks carefully.

The Open-Source Community Moat

Supabase has 73,000+ GitHub stars as of 2025. That number isn't just vanity. It represents:

- Free organic distribution (developers share what they star)

- Community contributions that improve the product without headcount cost

- Trust signal for enterprise buyers evaluating backend infrastructure

- Self-hostable option that keeps enterprise accounts who can't use managed cloud

The community also functions as a 24/7 support network. Supabase's Discord has hundreds of thousands of members. Questions get answered by other users before support ever sees them. That's a structural advantage on unit economics: your most vocal users become your support team without being paid.

Craft's internal thesis on Supabase states it clearly: "Devs have a high bar for community. Supabase proved that authenticity, open-source ethos, and developer-first culture aren't just nice-to-haves - they're moats."

You can't buy that. It accrues only to founders who genuinely care about the community because they came from it.

Enterprise Without Betraying Developers

One of the hardest transitions in developer tooling is going upmarket to enterprise without alienating the indie developers who built your reputation.

Supabase handled it cleanly. The core product stayed free and generous at the developer tier. Enterprise features - advanced SLAs (99.99% uptime), SOC2 and HIPAA compliance add-ons, dedicated VPC setups - were layered on top without touching the developer experience underneath.

The result: 1Password, PwC, and Johnson & Johnson are now publicly-disclosed enterprise customers. These aren't indie hackers running weekend projects. These are organizations with complex compliance requirements and procurement processes.

They came in because Supabase's open-source credibility was a trust shortcut. Enterprise buyers know: a product the developer community loves to this degree has been battle-tested in ways no marketing claim can replicate.

The AI Coding Boom: An Unexpected Multiplier

Supabase's 2024 - 2025 acceleration wasn't only organic. Something structural happened in the AI tools landscape that created enormous new demand for exactly what Supabase offers.

Cursor, Lovable, Bolt, v0, and other AI coding tools made it trivially easy to generate frontend code and full-stack applications in hours. The new vibe coder with no backend experience was suddenly shipping apps.

What every app needs: a backend. Auth, storage, a database, real-time updates.

Supabase's developer-friendly API and deep integration with AI tools made it the default backend choice for AI-generated applications. The Craft Ventures piece from 2025 is titled explicitly: "Inside Supabase's Breakout Growth: Lessons Scaling to 4.5M+ Devs, Powering AI Coding & Vibe Coding."

From 1M to 4.5M developers in less than a year. That's vibe coding demand landing on a platform that had spent four years being the right answer.

This is a compound effect most founders miss when thinking about growth. Building something genuinely useful attracts an audience. But if that audience expands suddenly due to external market forces - a new category, a new platform, a new behavior - the founders who built quality get the windfall.

You can't plan for the windfall. You can build something worth compounding.

What Supabase Did That Competitors Didn't

Let's be specific about the differentiation decisions that made this work.

1. Postgres, not a custom database. Betting on existing infrastructure with massive community momentum was a compounding choice. Every tutorial, Stack Overflow answer, and Postgres expert in the world became part of Supabase's flywheel.

2. Open source as default, not as a feature. Products that add open source as a feature don't get the community benefit. Products built as open source from the beginning attract contributors who improve the product for free.

3. Developer-built leadership. Paul Copplestone codes. The founding team codes. Product decisions come from people with genuine developer intuitions. That shows in the product quality and in community trust.

4. Activation obsession over acquisition obsession. Most funded startups optimize for top-of-funnel metrics because those are easy to present in board slides. Supabase optimized for activation depth. The downstream compound effect on retention and expansion revenue is what enabled the valuation growth.

5. Gradual enterprise expansion without developer tax. They didn't add "request a demo" buttons to the product or add sales friction for small teams. Enterprise was an option layered above, not a gate below.

Lessons for Indie Builders

Supabase's story is worth studying not because you're building the next $2 billion developer infrastructure company. It's worth studying because the underlying principles apply at any scale.

Lesson 1: Scratch your own itch, then instrument it. Supabase exists because Paul wanted this product. The authenticity that creates community trust starts with founders who are solving their own real problem. But authentic itch-scratching alone doesn't build a growth engine. Instrumenting it - finding the activation event, bifurcating the ICPs, measuring what actually compounds - is what converts passion into process.

Lesson 2: Find your activation event early. Not the sign-up. Not the email confirmation. The moment your product actually delivers its first unit of value. For Supabase it was database creation. For a task manager it might be the first task marked complete. For a writing tool it might be the first exported document. Everything in growth funnels backward from that event.

Lesson 3: Identify which ICP segment is failing silently. If you have multiple user types entering the same onboarding flow, the weaker segment is dropping out without telling you why. They're not giving feedback. They're just not coming back. The metric looks like aggregate churn when it's actually a specific cohort problem. Segmenting and serving them differently is unglamorous work with outsized impact.

Lesson 4: Open source community is underrated distribution. If your product can be open source, the distribution and trust flywheel you get from GitHub stars, community contributions, and self-host optionality is worth more than most paid channels at early stage.

Lesson 5: External tailwinds multiply existing quality. You can't control when AI coding explodes or when Firebase makes a frustrating policy change. You can make sure your product is worth scaling when the tailwind arrives.

Supabase's breakthrough came when they found the single signal hiding inside all the noise: database creation was the activation event that predicted everything downstream - conversion, retention, expansion. The hindsight version is always obvious, but living inside your own product you don't have that clarity. You have GA showing one number, Sentry logging errors you haven't triaged, App Store reviews mentioning something users keep saying, and no way to read all of it at once. Luka connects those sources, finds what they're saying together, and surfaces the one thing most blocking your growth at your current stage. You check it once in the morning and go work on what it tells you. See how Luka works.

Where Supabase Is Now

By early 2026, Supabase powers millions of databases worldwide, with tens of thousands created every day. The $5 billion Series E in late 2025 validated what the growth trajectory had been suggesting for two years: this is a generational developer tools company.

The competitive landscape has shifted. Supabase no longer competes primarily with Firebase. It competes for the infrastructure layer of the AI application stack - a category that didn't exist when Paul and Ant started building in 2020.

That's the compounding bet thesis in action. Build quality product. Build genuine community. Serve the activation event obsessively. When market forces create a new category, you're already the right answer.

The Bottom Line

Supabase didn't grow because of a go-to-market playbook. It grew because the product was genuinely better for a specific set of developers, the team was part of that community before they were building for it, and they instrumented the right things once the product was working.

The $2 billion valuation isn't the story. The story is the four-year compound: from $1M to $16M in revenue with a small team, a principled open-source decision, and obsessive focus on the moment a developer creates their first database.

That's replicable. Not the $2B valuation. But the thinking that got there.

The Developer Relations Flywheel

One growth mechanism Supabase executed that doesn't get enough attention: their Developer Relations engine.

Most dev-tools companies hire a few DevRel people to write tutorials and attend conferences. Supabase treated developer relations as a core product surface.

How it worked:

Every new Supabase feature launched with full documentation, video walkthroughs, and interactive examples. Not after release - on launch day. The mental model: if a developer can't use it independently in 30 minutes, the feature isn't shipped.

This created a compounding distribution dynamic. Developers who tried new features could share working examples immediately. Their Twitter posts, Stack Overflow answers, and blog posts became organic documentation that reached audiences Supabase's own channels never would.

The GitHub issues and Discord discussions also fed directly into product prioritization. Feature requests that appeared repeatedly from the community got built. This closed the loop between user feedback and product roadmap in a way most SaaS companies claim to do but rarely achieve at operational speed.

The result: A community that felt ownership over the product's direction. When you feel like you helped shape something, you defend it against competitors. You recommend it unprompted. You write tutorials about it without being asked.

That's not community management. It's product co-creation. The distinction matters because one produces brand affinity and the other produces genuine advocates.

The Numbers Behind the Valuation Leap

Supabase's $0.9B Series C to $2B Series D jump happened in seven months (September 2024 to April 2025). That's a 122% valuation increase in under a year.

The explanation isn't hype - it's metrics convergence.

By late 2024, three things arrived simultaneously:

- Revenue growth had inflected. The $11M to $16M jump from 2023 to 2024 showed the unit economics were working at scale.

- The vibe coding wave was clearly driving sustained demand, not a one-time spike.

- Enterprise adoption had crossed the credibility threshold with named logos (1Password, PwC, J&J).

When these three signals converge - accelerating revenue, structural tailwind, and enterprise validation - valuation jumps are rational. Investors are not paying for current revenue. They're paying for the next revenue curve.

This is also why Accel led the $200M Series D. This was infrastructure-layer investment thesis, not growth-stage SaaS. The investors who backed Supabase in 2025 were betting on the backend layer of the AI application economy, and Supabase had accumulated four years of developer trust that new entrants couldn't replicate with capital alone.

What This Means for Your Product

The growth story you just read has one implicit question running through it: which stage of your growth loop is actually the problem right now?

Supabase's answer was activation. Not acquisition, not retention - activation. They had sign-ups. They had a good product. What they had to optimize was the path between the two.

If you're working on growth, the answer for your product is specific to your data. You might have an acquisition gap, an activation gap, or a retention gap - and they require completely different responses. GA says one thing, your error logs say another, your app store reviews say a third. Correlating them manually is the task that never actually gets done.